Reasons Insurance Companies Get Involved with Your Roof

Insurance companies monitor roofs closely because they are the “first line of defense” for the entire property. Therefore, understanding the line between home maintenance and insurance coverage is key to protecting your investment. While gradual wear from sun, mold, or algae is considered the homeowner’s financial responsibility, insurance is designed to protect you from sudden, accidental damage. When a single weather event causes immediate damage, it falls directly within the province of your insurance coverage.

Old Age

The 10-15 Year Rule: Is your roof over a decade old? Many homeowners are blindsided when they receive a “mandatory roof replacement notice” in the mail. Because the risk of leaks increases significantly after this point, carriers often require a full replacement to prevent a sudden policy cancellation due to the roof’s potential for failure.

Wind Damage

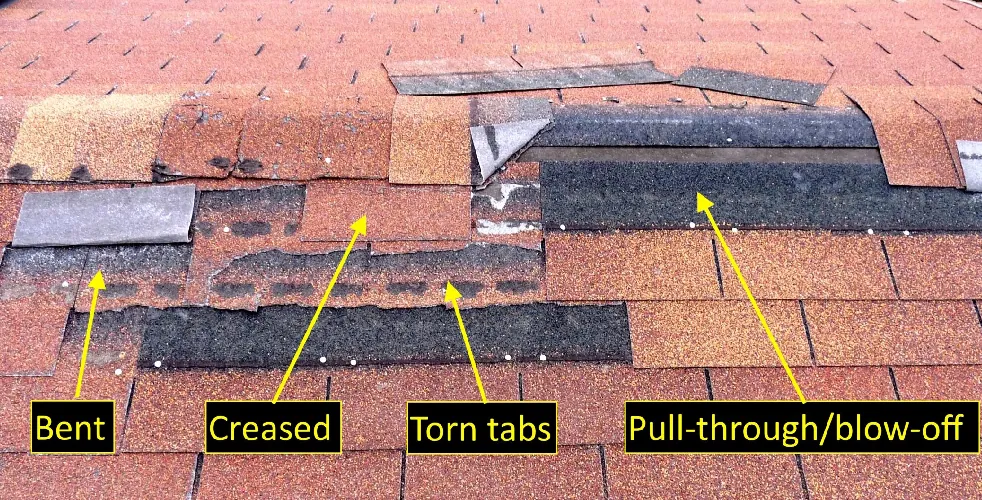

Creased or Missing Shingles: High winds can lift shingles, breaking the adhesive seal. Even if the shingle doesn’t completely blow off, a creased or torn shingle is considered structural damage because its waterproofing ability is compromised. A single wind event causing damage is generally covered by most insurance policies.

Hail Damage

Impact Bruising: Hail doesn’t have to put a hole in the roof to warrant a claim. Large hail knocks the protective granules off the shingles, exposing the asphalt matting to UV rays. Even though this “bruising” often looks superficial, it can deteriorate rapidly, causing leaks. To cause significant damage covered by most insurance, hail usually needs to be larger than 1″.

Falling Debris

Limbs & Leaves: Impact damage during a storm from overhanging tree branches or falling limbs is a standard “peril” covered by most insurance policies. However, cumulative minor damage not related to a specific storm is usually paid for by homeowner.

💡 Expert Insight: It surprises many homeowners to discover that a “30-year” shingle isn’t necessarily good for 30 years in the eyes of their insurer — or in Florida’s climate. The combination of relentless UV rays, year-round humidity, and hurricane season puts roofs here under far more stress than in most of the country. As a result, insurance providers may issue a replacement mandate or threaten to cancel your policy once your roof reaches 10+ years old, regardless of how it looks from the street.

Insurance Claims & Your Roof: What You Need to Know

Filing a claim is a significant decision that impacts your property’s history and your future premiums. To make the most of your coverage, it is important to understand the mechanics of how claims are filed and documented. Use the breakdown below to learn how to transition from discovering storm damage to securing a professional replacement with the help of expert documentation.

Who Pays for the Roof?

💡 Expert Insight: If a roof leak causes damage to your drywall, insulation, or flooring, the insurance company gets involved not just for the roof, but for the consequential damages inside the home. This is called Interior Secondary Damage. But if you didn’t report the leak or storm damage in a timely manner, this secondary damage may not be covered by insurance.